Online banking has delivered financial inclusivity and profits, but has it also created shared value?

In April 2022, there was a sense of optimism at MYbank, an Ant Group-backed company, which had reported year-on- year growth of 32 percent for the first quarter, a significantly higher number than that for the same period in 2021. Moreover, its total loans and advances for the first quarter was a staggering US$30 billion1.

Established in 2014 following a change in regulation that allowed selectively-licensed private banks to operate in China, MYbank had created a successful business model, using technology as its magic wand. It operated purely online, and largely focused on small- and medium-sized enterprises (SMEs) and rural farmers, who were hitherto unserved or underserved by formal financial institutions.

Banking had traditionally paid more attention to high-net- worth individuals (HNWI), and concentrated on having fewer accounts and more one-on-one relationships. However, MYbank had decided to direct its attention to technology to enable quick transactions, handle a large volume of low-income consumers, and lower operational costs to create a sustainable business model. Its strategy was to use automation, standardisation, and Artificial Intelligence (AI) to reach a very large number of customers with low balances.

It was the large volume of such customers without access to formal financial lending that proved to be the ticket to MYbank’s success. There were many examples of inclusive finance models implemented globally, but very few could match the scale of MYbank. For example, Bangladesh’s Grameen Bank, the pioneer in inclusive finance, had 9.33 million members in 2020 after more than a decade of existence, while MYbank had more than 70 million users by 2021, only six years after its inception.2

However, in 2022, the contracting Chinese economy posed a concern for MYbank’s future growth. Separately, competition in the online banking market was cut-throat, with competitors like Tencent-backed WeBank encroaching into MYbank’s market space. Additionally, the COVID-19 pandemic had negatively affected its target customers. In response, MYbank cut interest rates for its microloans, while also using strategies like cost optimisation and economies of scale to offset the impact of interest cuts on profits.

How could MYbank’s business model allow it to remain competitive amidst market pressure while delivering shared value? This was a classic scenario where a trade-off needed to be made between profit and social responsibility.

TARGETING THE FINANCIALLY INVISIBLE

In 2014, the China Banking Regulatory Commission (CBRC) introduced new regulations to promote inclusive finance and allow privately-owned organisations to operate in the banking sector to serve the low-income population. The concept of inclusive finance had originally emerged from the analysis of challenges posed by the unequal distribution of wealth across the world, more or less in line with the 80/20 Pareto principle. In China, the equation was similar–traditional banking institutions were focused on the HNWI customers who made up 20 percent of the population but controlled 80 percent of the country’s wealth and resources.3 The remaining 80 percent of the population, which included 45 percent of the country’s population who lived in rural areas, were marginalised and found it harder to get formal credit access.4 This was partly due to the high overhead costs of branch banking which forced banks to focus only on market segments that offered the highest margins. Besides, only one third of the population in China had credit records while the rest were ‘credit-invisible’, and loans from rural areas accounted for only 23 percent of the country’s total loan balance.5

However, smartphone penetration rates in China were high. By 2015, 49 percent of the country’s population were active Internet users, and SMEs and small consumers were already engaging with e-commerce platforms like Alibaba, Taobao, and T-Mall. Promotion and sales of agricultural products on the Internet using e-commerce had also become commonplace.6 Such data encouraged MYbank to look at the possibility of introducing mobile-based banking products for small value customers.

MYbank’s ‘310’ MODEL

In 2015, MYbank established an online-only platform that enabled SMEs to open accounts and apply for loans quickly and easily, without the need for extensive paperwork or physical branches. Big data and AI were used to assess the creditworthiness of applicants, allowing for quicker and more accurate lending decisions. It also harnessed technology to streamline its operations, reduce costs, and provide faster and more efficient services.

These technologies were clubbed together with an internally-developed lending model called the ‘310’ model, which included more than 100,000 risk profiling metrics and 100 credit risk models specifically suited to SME and individual lending. It took just three minutes for a customer to apply for a loan, demanded zero collateral, and the loan could be approved within one minute. The model was developed through iterative testing and refining, and assessed loan applications using built-in algorithms to weigh various risk parameters like limited credit histories, unreliable income streams, and default risk. It also used the data of consumer repayment records from e-commerce platforms like Alibaba and Alipay, smartphone payment records, registered online customer profiles, e-commerce transactions, local government records, and insurance records to assess loan applications. The ‘310’ model incorporated algorithms for monitoring loans and their risk of default using online tracking methods, and could assess monthly sales of small businesses and predict their repayment patterns.

Although the loans were extended without any collateral, the interest rates charged were competitive, ranging from six to 14 percent.7 ‘310’ was profitable, partly because of lower operational and delivery costs, generating net interest margins of three to five percent. This was considerably higher than those of China’s biggest commercial banks.8 For example, a traditional bank spent about RMB 2,000 (US$294) to process a micro loan, whereas MYbank’s average loan cost was around RMB 2.30 (US$0.34).9 Additionally, the bank’s return on equity (ROE) was at 13.4 percent, which was slightly above the 13.1 percent average of traditional banks in China.10

The simplicity and ease of use of the ‘310’ model helped boost loan approval rates, which quickly rose to four times those of traditional lenders (which typically rejected 80 percent of SME loan requests and took at least 30 days to process the applications), and also helped limit MYbank’s average non-performing loan (NPL) ratio to about one percent.

Providing SME support

By 2020, MYbank was able to service over 35 million SMEs (refer to Figure 1). The duration of the loans, on average, was approximately up to 90 days, and customers could flexibly borrow money and pay back the loans on a rolling basis. The average loan amount granted was RMB 34,000 (US$4,850). Analysis of the loan data revealed that about eight percent of the loan applications were submitted between 11 pm and 4 am, when traditional banks in China were closed for business, reflecting the need for 24/7 financial access by small entrepreneurs. The bank also tried to support green business practices by applying preferential interest rates for SMEs that implemented green initiatives, and such tracking of green businesses was also built into the automated loan approval process.

MYbank captured almost half of the SME market in China, and about 78 percent of these customers were first-time borrowers and 40 percent were female-run SMEs.11 The bank’s success in the SME market became a strong source of motivation for other Chinese banks to boost their SME lending. Soon, state-owned enterprises like China Construction Bank increased their small business lending, while private firms like Tencent Holdings and Ping An Insurance Group started to introduce similar services for SMEs.12

Promoting agriculture through farmer loans

MYbank also extended loans to farmers in support of the state agenda to promote agriculture as the government was concerned that the country, which was the world’s largest food importer, did not produce enough food to meet domestic consumption. Geographically, only 13 percent of the total land in the country was arable, but this came under constant pressure due to heavy industrialisation and urban encroachment. The Chinese government had introduced strict farmland protection measures and drawn ‘red lines’ to protect the country’s farmlands from industrial encroachment.13 Over the past decade, China had tried to ramp up its own food production to reduce its dependency on imports by introducing higher-yield grains, improving farming techniques, and implementing privatisation policies to incentivise farmers. However, the country still lagged in yield and food safety relative to developed countries with robust agricultural sectors. In addition, ageing rural demographics, environmental degradation, climate change, groundwater depletion, heavy metal pollution, and a lack of technological adoption also posed challenges to its agricultural sector, which employed around 350 million people as of 2021.14

MYbank’s farmer loans were therefore considered a boon, as they could provide the much-needed capital boost to the ailing sector. The loans were of short duration–around 90 days like that for SME loans–and delivered in collaboration with numerous other financial institutions that served as sources of capital.15 Farmers could borrow and repay at any time, and interest was calculated based on the duration of the loan. There were no penalty interest charges or fees for early repayment and the credit limit was restored in real time once the repayment was made.

To deliver these farmer loans, MYbank combined its ‘310’ model with an in-house AI solution called ‘Tomtit’, which used satellite remote sensing and image recognition to grant and monitor loans. To apply for a loan, farmers could download the MYbank app on their mobile phones, authorise the application for information inquiry, select their farmland plot (also known as the act of ‘circling’), and then receive the loan within a few minutes. As a risk control measure, Tomtit checked for pre-existing records of the applicant on other platforms like Alibaba’s Taobao and Alipay for an accurate understanding of the customer’s financial situation.

Using publicly available satellite images and images provided by farmers, climate data, industry patterns, land registration data from government agencies, and information about factors affecting crop price and expected crop growth, Tomtit could estimate the yield and output value of the selected land, and accurately evaluate risk. This unambiguous risk analysis method provided reasonable levels of credit and an appropriate repayment plan to farmers based on the risk scores generated. As the borrowing cycle was short, users were less sensitive to interest rates and more concerned about whether the loan amount was sufficient to meet their needs. After loan disbursement, Tomtit constantly monitored the farmlands using satellite images to assess the growth and condition of the crops, and predict any likely risk of loan default. The satellite images were updated in real-time in a cycle of five to seven days for MYbank to make precise assessments, and proactively manage risks.

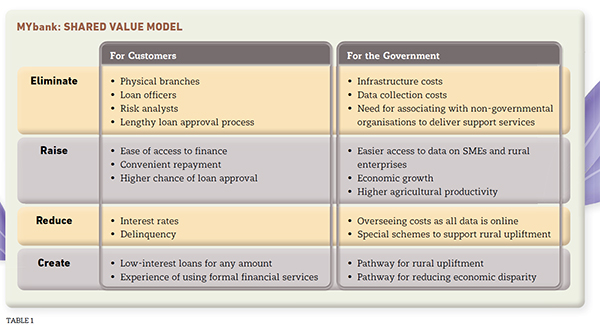

CREATING SHARED VALUE

Through its banking services, MYbank tried to create shared value for all its stakeholders and fulfil its corporate social responsibilities (CSR) while addressing the triple bottom line of people, planet, and profit.

For example, in 2020, MYbank implemented a series of measures to help SMEs overcome the economic impact of the COVID-19 pandemic, including waiving or lowering interest rates. It also collaborated with 100 banks to support SMEs as they resumed operations post-pandemic. Consequently, it was able to serve over 10 million SMEs and extend loans totalling RMB 400 billion (US$63 billion). A ‘zero-payment-day’ service was launched, which attracted around 6.5 million rural lenders in one month, and this was extended by another four months.

The bank also established strategic goals to help develop China’s green financial system and green financial instruments, promote participation among consumers and investors in green finance, and guide SMEs and farmers to use green finance as a means of delivering on China’s broader green production and consumption goals.16

MYbank’s business model hoped to illustrate how inclusive finance could address economic, social, and environmental risks by empowering vulnerable populations to build resilience and mitigate the impact of climate change. The World Bank’s research had stated, “While the poor suffer disproportionately from climate change, they have the smallest margins and least access to resilience strategies that can help them avoid, absorb, and adapt to shocks. Rural MSMEs (micro-, small- and medium-sized enterprises) are vital to the health of the rural economy and global food security. These MSMEs, which include primary producers, processors, and traders, face increasing income and asset loss risks due to the changing climate and more frequent natural disasters, and are often not equipped to absorb the economic effects of losses from climate change.”17 MYbank had taken several initiatives to offer its digital financial services in building climate resilience. For example, in 2021, it worked with China Agricultural University to assist the National Disaster Reduction Committee in controlling the flood situation, creating a model to measure the flood and depicting what each area looked like, and advising how to evaluate the economic loss.

MYbank had also launched social welfare programmes to reduce the economic disparity faced by women. According to the International Finance Corporation, women entrepreneurs in emerging markets faced a daunting gender finance gap when it came to growing their start-ups, as they continued to experience unequal access to capital in the traditional banking and investment environment. MYbank tried to bridge this gender bias through a ‘3D’ approach, by enabling digital financing, providing digital skills training, and building digital communities for women entrepreneurs. Between 2015 and 2020, MYbank was able to provide financing to more than 8.2 million women-operated SMEs in China, with an average loan amount of US$5,700. By 2020, over 50 percent of MYbank loan recipients were women entrepreneurs, and about 80 percent of them had received their first-ever loan from the bank.

PROFIT VERSUS MOTIVE

In April 2022, as China’s rural economy started to slowly recuperate after the pandemic, MYbank’s role as an enabler of rural entrepreneurship became even more critical amidst rising regulatory control to support stricter oversight on data sources and data use.18 At the same time, competition in the online banking market was increasing, and players like WeBank were encroaching into the SME market space.

A separate consideration was regarding digital currencies. In January 2022, China launched its pilot digital yuan, also referred to as the e-CNY, which was highlighted by international and national institutions as a tool to promote an inclusive digital economy. MYbank had been selected as one of the distributors of e-CNY, which required residents in China to link their e-CNY services to a bank account. The e-CNY was expected to have a symbiotic relationship with payment platforms like Alipay and WeChat Pay, and provide benefits to online payment platforms by creating more visibility and generating additional payment flows.19 The challenge was in appreciating its relevance to MYbank’s target consumers, and how it would impact the bank’s existing business and solutions.

Despite tugging tensions, the future looked promising. But while MYbank’s capability of creating shared value was substantial, its profit-making goals were also a necessity. On a pessimistic note, increased competition and regulatory changes could potentially erase some of the bank’s competitive advantage. Moreover, its upper hand in creating technological solutions could fade over time, as competitors came up with similar solutions. However, with the growing penetration of technology in rural China, and continued government support for microfinance, it was unlikely that MYbank would need to succumb to trade-offs on social responsibility and sustainability over profit.

Dr Heli Wang

is Dean, College of Graduate Research Studies, and the Janice Bellace Professor of Strategic Management, Lee Kong Chian School of Business at Singapore Management University

Lipika Bhattacharya

is Assistant Director at the Centre for Management Practice at Singapore Management University

This article is based on the case study ‘Ant Group-Backed MYbank: People, Planet, Profit in Rural China’ published by the Centre for Management Practice at Singapore Management University. For more information, please visit https://cmp.smu.edu.sg/case/5576 or scan the QR code below

Endnotes

1. US$1 = RMB 6.36 as of March 2022.

2. “Bank for the Poor”, Grameen Bank.

3. “Macro-Finance Salon (No. 56) and Fintech Open Classes (No. 3): Financial Technology Promotes Inclusive Finance”, International Monetary Institute, April 19, 2017.

4. “Statistical Communiqué of the People's Republic of China on the 2014 National Economic and Social Development”, National Bureau of Statistics of China, February 26, 2015.

5. Tim Tsang, “How New Credit Scores Might Help Bridge China's Credit Gap”, Center for Financial Inclusion, June 6, 2016.

6. Simon Kemp, “Digital 2015: China (August 2015)”, DataReportal, August 18, 2015.

7. Niclas Benni, “Big Data and Automated Credit Scoring in Rural Finance: The Case of MYbank”, Rural Finance & Investment Learning Centre, November 19, 2020.

8. Shu Zhang and Ryan Woo, “Alibaba-Backed Online Lender MYbank Owes Cost-Savings to Home-Made Tech”, Reuters, February 1, 2018.

9. SME Finance Forum, Annual Report 2019.

10. Ibid.

11. Ibid.

12. Ibid.

13. David Stanway, “China's Total Arable Land Shrinks Nearly 6% from 2009- 2019–Survey”, Reuters, August 27, 2021.

14. Lillian Li, “Prediction: Agriculture Tech is Going to be Big in China”, Chinese Characteristics, December 10, 2021.

15. “Alipay’s Xiang Hu Bao Online Mutual Aid Platform Attracts 100 Million Participants in One Year”, Business Wire, November 27, 2019.

16. Gilbert + Tobin, “Green Finance Taking Root funding Australia's Transition to a Low Carbon Economy”, Lexology, May 18, 2017.

17. Juan Buchenau, “Climate Smart Financing for Rural MSMEs: Enabling Policy Frameworks–G20 Global Partnership for Financial Inclusion”, The World Bank.

18. “China Regulator Finalizes Guidelines on Banks’ Internet Loan Businesses”, Reuters, February 20, 2021.

19. Richard Turrin, “China’s Digital Yuan is Not Death Knell for Alipay and WeChat Pay”, South China Morning Post, February 15, 2022.