Financial inclusion or providing access to and enabling active usage of affordable financial products and services, is a global and pressing issue that, over the last 30 years, has received a lot of attention from multilateral development banks, government bodies and NGOs. According to the World Bank, there are two billion people, or about half of the global adult population, and 200 million micro, small and medium enterprises (MSMEs) that do not have access to formal financial products and services. With small transaction sizes and limited credit history, financial institutions view these individuals and businesses as too expensive and risky to serve. An additional challenge is that many of these potential clients are located in remote rural areas with limited infrastructure. The majority of them are at the ‘Base of the Pyramid’ (BoP) earning less than US$2 per day, and rely on informal means to borrow money such as pawnbrokers, payday lenders and loan sharks that are often extremely expensive and unreliable.

This situation gives rise to one of the greatest paradoxes in today’s world: the people with the most limited resources are the ones paying the highest fees for financial products and services. Therefore, providing access to affordable financial products to the unbanked has tremendous potential to help them improve their social and economic status. In fact, it has been widely studied and documented that financial inclusion allows households to expand consumption, manage risks and invest in durable goods, health and education, thereby reducing poverty and increasing economic development.

Digital financial services as a key enabler to financial inclusion

How to best solve the financial inclusion problem? The answer may lie in advances in digital technologies. Mobile phones, cloud computing, big data analytics, artificial intelligence and blockchain are making it possible for anyone to access financial products and services for the first time, wherever they are and whenever they need them, in a faster, cheaper, more transparent and efficient way than traditional banking. According to a McKinsey report published in September 2016, mobile technology can lower the cost of providing financial services by 80 to 90 percent, enabling banks and financial institutions to potentially serve the BoP in an economical way.

Another interesting statistic comes from GSMA, a global organisation that represents the interests of more than 800 mobile operators worldwide. Its website states that mobile phone penetration rate in most emerging market countries averages around 80 to 85 percent as of 2016, even though the average banked adult population in these countries may be well below 40 percent. Therefore, the mobile phone has become a key tool to access financial products for the unbanked and MSMEs.

How do you implement these new technologies to drive financial inclusion? Fintech startups hold the key to driving higher financial inclusion in emerging markets. A small subset of these startups is taking the lead in doing it through innovative products and business models. A good example, which is often quoted, is M-Pesa, a Kenya-based startup founded in 2006 that uses the mobile phone to transfer money domestically as well as make payments. The startup has been highly successful, with more than 84 percent of Kenyans who are living in poverty using its services, and 40 percent of Kenya’s GDP going through the company. M-Pesa was able to grow very quickly, achieving one million customers in just eight months, and is now serving 16.6 million active customers, or 36 percent of the country’s population. These figures are impressive and beg the question: What are the key factors that make M-Pesa so successful?

Understanding the factors that make Fintech startups like M-Pesa successful is essential to it being replicated and used by others. Researchers and academics have identified many factors. For instance, Lee and Teo (2015) developed the LASIC Principles representing five factors—Low Margins, Asset Light, Scalable, Innovative, and Compliance Easy—that Fintech companies need to have in order to drive higher financial inclusion. They supported these factors through case studies; M-Pesa was one of them. While my research focuses on key success factors that Fintech startups need to have to drive higher financial inclusion, it is one of the first studies that quantifies the effects of these factors. Quantifying the effects allows for a better appreciation of which factors are more important for financial inclusion and financial performance.

Identifying and quantifying success factors for Fintechs in financial inclusion

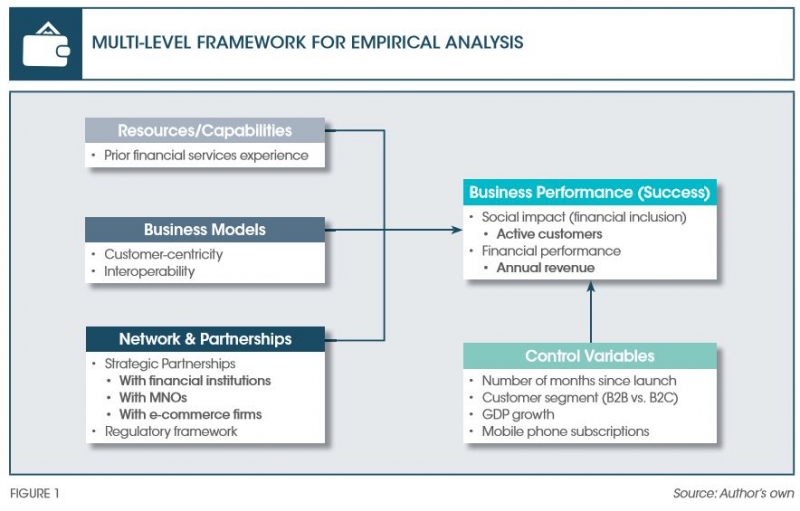

To determine which factors are most essential for Fintech startups in order for financial inclusion to be successful, I developed a multi-level framework of factors through the perspective of strategic management theories. In particular, I examined how factors related to different aspects of a company’s business model, internal resources/capabilities, strategic partnerships, and the market/environment affect the success of new ventures, as measured by financial performance and financial inclusion.

I identified and evaluated five key success factors from the multi-level framework presented in Figure 1.

• Prior financial services experience of the founding team;

• Degree of customer-centricity in the startup’s business model;

• Whether the startup has an interoperable business model;

• Strategic partnerships (with three types of institutions); and

• Openness of the regulatory environment to financial inclusion.

An important consideration of the multi-level framework and the analysis performed is the definition of success. In this case, success is defined as achieving a dual goal of delivering social impact through higher financial inclusion and being a sustainable business through higher financial performance. Therefore, for a Fintech startup to be considered successful, it would have to meet these two criteria.

Based on empirical analysis of objective, measurable data collected through extensive interviews from 63 Fintech startups that are serving the unbanked across Southeast Asia, India and Africa, I find that three out of the five factors evaluated have a significant and positive correlation with financial performance and financial inclusion in these startups: founders/founding teams with prior financial services experience; the degree of customer centricity in the company’s business model; and strategic partnerships with financial institutions and e-commerce firms all seem to be highly correlated and present with successful firms.

INDUSTRY EXPERIENCE OF FOUNDING TEAMS

Having a founder/founding team with prior financial services industry experience seems to provide the company with a better understanding of the key issues and problems that need to be solved and thus the ability to develop products that customers really need. This experience is essential in the financial services sector, which is highly complex and highly regulated. The empirical model showed that this factor leads to higher financial performance, but it may not contribute to higher financial inclusion. An example from my research study is JUMO, a South African-based Fintech startup that uses behavioural data from mobile usage to create financial identities for, as well as offer financial products to MSMEs that did not have prior access to formal financial services. The company’s founding team has more than 35 years of combined experience in the financial services sector. For a founding team of four people, this represents an average of approximately 8.5 years per member, which is significantly higher than the average industry experience from other Fintech startups in my data sample.

DEGREE OF CUSTOMER-CENTRICITY

Customer centricity refers to having a business model that is solely focused on solving the customer’s needs. The positive effects of having a customer- centric business model have been studied extensively in the marketing field, but mainly in the context of large corporations. My research shows that customer centricity is equally important in Fintech startups for financial inclusion. Furthermore, multilateral development organisations such as the Consultative Group for the Advancement of the Poor (CGAP), the International Finance Corporation (IFC, the private arm of the World Bank), and Accion have established that adopting a customer-centric business model is important in driving higher financial inclusion, since there is a large disconnect between poor people who have registered for formal bank accounts and digital financial services accounts on mobile phones and those who actively use them. Active usage is defined performing at least one transaction using the startup’s product/service within a 90-day period. According to GSMA, as of 2015, more than two-thirds of digital financial services accounts on mobile phones that have been registered worldwide are inactive, representing an active ratio of 32.6 percent.

The empirical analysis expands on the work that CGAP has done by developing a customer centricity score that Fintech startups can use, and empirically demonstrating its impact on financial inclusion and financial performance. The analysis highlights that financial inclusion (as measured by active customers) is highly sensitive to customer centricity, but this is not so much the case for financial performance. Customer centricity may provide a signal to the strategy of these Fintech startups—by focusing on living their customers’ problems and needs, these startups acquire a larger customer base and achieve financial sustainability in the future. A Fintech startup in my research study, which has a highly customer-centric business model, is Wave Money, a Myanmar-based company that offers money transfers and payments through the mobile phone. From its inception, Wave Money recognised that serving the unbanked requires a real understanding of their behaviour and needs, and thus leveraged the principles of human-centred design to build their mobile application for their customers.

LEVERAGING STRATEGIC PARTNERSHIPS

The importance of strategic partnerships on financial performance and financial inclusion for Fintech startups serving the unbanked is also emphasised in my research results. Both financial inclusion and financial performance were highly sensitive to partnerships with financial institutions and e-commerce firms, while partnerships with mobile network operators (MNOs) did not appear to impact the success of these startups. Since mobile phones are the main tool to help drive financial inclusion for the poor, one can expect to see that alliances with MNOs would significantly impact the startup's financial performance and drive higher financial inclusion. However, this was not the case. One way to explain this result is based on the size of the MNO. If the MNO has a significant, controlling market share (more than 60 percent) in a country, then partnerships with multiple MNOs may not be necessary.

A good example of partnering with financial institutions is MicroEnsure, a U.K.-based provider of microinsurance products serving more than 28 million active customers in 15 countries across Africa, India and Southeast Asia. MicroEnsure currently partners with 90 insurance providers and microfinance institutions globally, and this has been a critical ingredient for its success. The partnerships between Fintech startups and financial institutions is a topic that has received a lot of attention recently, with the announcement that the Monetary Authority of Singapore and the IFC have set up the ASEAN Financial Innovation Network to help build collaboration between Fintech startups and financial institutions that are focused on driving higher financial inclusion in the region. An interesting outcome of the research study is that strategic partnerships with e-commerce firms are important, highlighting how the Internet is becoming an important distribution channel that Fintech startups should exploit to access more customers and drive higher financial performance.

Beyond empirical analysis

Illustrative case studies of four Fintech startups in my data sample that were considered successful complemented the empirical analysis performed in my research study. These case studies showed that additional factors such as scalability, funding from well-known investment firms and development organisations and prior startup experience could also contribute to driving higher financial inclusion and higher financial performance for Fintech startups serving the unbanked. 'Pull' vs. 'push' products can also influence the customer adoption rate and ultimately impact the company's financial performance.

To achieve greater financial inclusion and financial performance, the case studies demonstrated that it was important for these Fintech startups to have a business model that can quickly scale up and reach as many customers as possible within a short time frame. For instance, by serving five million active customers in eight countries within a span of less than two years, JUMO has shown that it has a highly scalable business model.

Funding from well-known investment firms and development organisations such as the IFC has proved to be an important factor in the success of Mobisol, a German- based off-grid solar panel leasing company that operates in three African countries. Customers can get a low interest rate from Mobisol to finance the solar panel and pay digitally through their mobile phones. By building a credit profile from customers through the leasing of solar panels, Mobisol will eventually offer other financial products and services such as insurance and savings accounts. In 2016, the IFC invested €5.4 million (US$6.75 million) in Mobisol. While the amount of funding is helpful, the brand name and recognition from the IFC increased Mobisol’s credibility and boosted its brand, resulting in higher customer trust and more customers. Moreover, the development organisations also helped open doors to more resources that the firm may need, ultimately improving its financial performance.

Finally, the type of product sold can impact the financial performance and financial inclusion of new technology ventures serving the unbanked and underbanked. ‘Pull’ products refer to items that are necessities people use on a daily basis, such as transportation, electricity and food. ‘Push’ products, on the other hand, are goods and services that have less obvious value or that provide uncertain benefits in the future, such as loans, savings, insurance, etc. Organisations that sell pull products do not have to spend a lot on marketing to convince customers to adopt their products, resulting in a less customer- centric business model. In Mobisol’s case, providing electricity to customers via solar panel systems is effectively a pull product, and thus a key reason why the company has been successful.

Recommendations

My research study offers quantitative support to new factors such as customer centricity, as well as other factors like strategic partnerships and prior financial services industry experience, which play a key role in financial inclusion and financial performance. The empirical models have immediate practical applications for venture capital firms and investors, which evaluate new technology ventures in financial inclusion by providing a quantitative, data-driven methodology that complements their internal methods. For Fintech founders, the empirical models give them clear guidelines on what factors they should be focusing on to increase their chances of success. Moreover, the models also show which factors have a greater impact on financial inclusion and financial performance.

Dr. Miguel Soriano

1. Arjuna Costa & Tilman Ehrbeck, “A Market-Building Approach to Financial Inclusion. Innovations: Technology, Governance, Globalization”, 2015.

2. Asli Demirgüç-Kunt, Leora Klapper, Dorothe Singer & Peter Van Oudheusden, “The Global Findex Database 2014: Measuring Financial Inclusion around the World”, World Bank Policy Research Working Paper 7255, 2015.

3. GSMA, “2015 Mobile Insurance, Savings & Credit Report, Mobile for Development”, 2016.

4. David Lee & Ernie Teo “Emergence of FinTech and the LASIC Principles”, SSRN, 2015.

5. Roger T. A. J. Leenders & Shaul M. Gabbay, “CSC: an Agenda for the Future”, In Corporate Social Capital and Liability (pp. 483–494), 1999.

6. James Manyika, Susan Lund, Marc Singer, Olivia White, & Chris Berry, “Digital Finance for All: Powering Inclusive Growth in Emerging Economies”, McKinsey Global Institute, 2016.

7. Peer Stein, Oya Pinar Ardic & Martin Hommes, “Closing the credit gap for formal and informal micro, small, and medium enterprises”, 2013.